")

Buying a home is rarely just a transaction. It is a moment of intent — a decision to put down roots, to invest, or to return to something familiar. In Jamaica, that decision unfolds within a framework of law, custom, paperwork, patience, and no small measure of trust. On the surface, it may appear straightforward: find a property, agree a price, sign the papers. But beneath that surface lies a carefully sequenced process, shaped by legislation, government agencies, professional practice, and the realities of time.

Too often, buyers and sellers step into this process with only fragments of information — a headline tax rate here, a bank estimate there — only to discover later that costs, timelines, or responsibilities were misunderstood. The result is stress, delay, and, in some cases, avoidable financial strain.

This guide is designed to strip away that uncertainty. It sets out, in clear terms, the key stages involved in purchasing real estate in Jamaica, the typical costs faced by both buyer and vendor, and the legal and administrative steps that bring a transaction to completion. Whether you are purchasing with cash, arranging a mortgage, or selling a property you’ve owned for years, the aim is simple: to help you understand what is likely to happen, when it happens, and why it matters.

Because when you know the process, you are not merely reacting to it — you are navigating it.

Important disclaimers (read first)

Rates and fees can change by Government policy (Budget/revenue measures) and by agency fee schedules. Always re-check at the time of your transaction (especially if you’re closing months after signing).

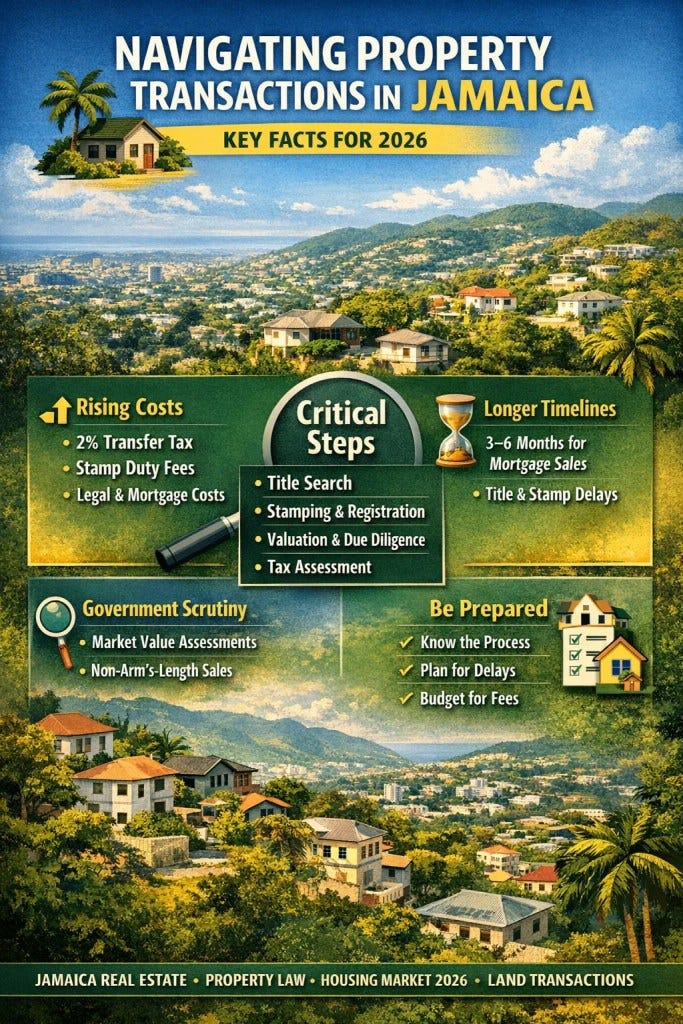

The Stamp Office can assess taxes on the “market value” (not only the stated price), especially where the transaction is not at arm’s length (e.g., gifts) or where consideration is unclear.

Professional fees (attorney, valuation, survey, agent) are market-based and can vary widely depending on property value, complexity, location, title issues, and urgency.

Bank / lender fees vary by institution and change over time; always request the lender’s written fee guide/loan estimate.

1) Key stages in buying a home in Jamaica (2026)

StageWhat happens (practical)1. Prequalification / pre-approval (if borrowing)Lender checks income, liabilities, credit, deposit, and affordability. Timelines vary by lender and the completeness of documents.2. Property search & offerYou negotiate price, timeline, inclusions (appliances, fixtures), and conditions (subject to financing, subject to valuation, etc.).3. Agreement for SaleAttorneys prepare/review and both parties sign. Deposit commonly ~10% by practice; see note below. 4. Deposit paymentTypically paid to the vendor’s attorney and applied toward taxes and completion.5. Title search & due diligencePurchaser’s attorney checks ownership, encumbrances, caveats, property tax status, boundaries/plan issues, strata matters, and any red flags.6. Stamping (Stamp Office)Agreement/transfer documents go to the Stamp Office for assessment; taxes are paid after assessment instructions are issued. – JIS7. Lodge transfer for registrationTransfer is lodged at the Titles Office/Registrar of Titles for registration.8. Completion / possessionBalance is paid, keys/possession handed over, closing deliverables exchanged.9. Mortgage registration (if applicable)Lender’s mortgage/security is registered against the title.

Deposit “rule” (disclaimer)

10% deposit is widely treated as “customary” in Jamaica, but the law historically referenced 7.5% as an implied minimum term in certain contexts (and practice doesn’t always align perfectly with that section). Treat this as a legal drafting issue to be handled by the attorneys, not a DIY rule.

2) Government taxes/fees that most people must budget for (2026-verified)

Transfer Tax (Vendor pays, in most standard sales)

Transfer Tax: 2% of the value (typically the purchase price/consideration, but can be market value in some cases).

Stamp Duty (usually shared)

Stamp Duty moved from ad valorem to a flat rate for most relevant instruments. For typical property transactions at or above the threshold, the commonly applied figure is J$5,000 per document, and it’s often shared between vendor and purchaser (commonly J$2,500 each).

Disclaimer: The Stamp Office can apply different flat rates in lower-value cases and may treat document sets differently; your attorney confirms what applies to your file.

Registration fee (transfer) — shared

Registration fee for the transfer is 0.5% of the consideration, and it is commonly shared between purchaser and vendor (effectively 0.25% each).

3) Vendor’s costs (Seller) — updated & corrected

Core “official” items most vendors face in a normal sale

Transfer Tax: 2% (vendor)

Stamp Duty: commonly split; vendor share often J$2,500

Registration fee (transfer): commonly split; vendor share often 0.25%

Market/practice items (vary by deal)

Real estate agent commission: commonly 5% of sale price (if an agent is used).

Plus 15% GCT on the commission (so 5% becomes 5.75% all-in).

Attorney fees: widely variable (often quoted as a % of the sale price, but not fixed by law). Use your attorney’s engagement letter as the source of truth.

Vendor cost disclaimer: Your “~11.8%” headline can be true in some commission-heavy scenarios, but it is not a statutory total—it depends heavily on commission + legal fees and whether the vendor is paying for extras (repairs, strata arrears clearance, etc.).

4) Purchaser’s costs (Buyer) — updated & corrected

Core “official” items most buyers face

Stamp Duty: commonly split; buyer share often J$2,500

Registration fee (transfer): commonly split; buyer share often 0.25%

Due diligence items (often necessary, but not “government taxes”)

Valuation report: varies by lender/valuer and property type.

Surveyor/ID report (where required): varies by property and whether boundaries/plan issues exist.

Attorney fees: variable (complex titles, strata issues, family land, missing documents can increase costs).

Buyer cost disclaimer: For cash purchases with clean title, the buyer’s “all-in” costs can be relatively modest; for complicated titles or tight timelines, legal and due diligence fees can rise quickly.

5) Mortgage-related costs (Buyer) — corrected for 2026

Here’s what most buyers miss: there are (A) Government registration/taxes and (B) lender fees.

A) Government-side mortgage registration/taxes

Mortgage registration fee: commonly 0.5% of the loan amount (not the property value).

Stamp Duty (mortgage/security documents): Government policy replaced ad valorem stamp duty with a flat rate stamp duty per document, including for security/collateral documents.

Disclaimer: Banks sometimes present a blended figure because they bundle copies/ancillary documents/administration—so the “stamp duty line” on a bank estimate may not look like a simple J$5,000.

B) Lender fees (vary by institution)

Common examples include:

Processing / application / commitment fees: lender-specific (ask for the fee guide).

Bank legal fees / documentation fees: lender-specific; sometimes added to the loan.

Insurance: lenders typically require property insurance; mortgage-related life/credit insurance depends on lender and borrower profile.

Mortgage disclaimer: Because lender fees differ so much, it’s risky to publish a single “mortgage pushes costs to X%” number as a universal truth. A better approach for 2026 is: “Mortgage costs can materially increase closing costs; get a written loan estimate from your lender and compare 2–3 institutions.”

6) Timeline (still broadly accurate, but add real-world caveats)

Cash purchase

30–90 days is realistic if title is clean and both attorneys are responsive.

Delays usually come from title defects, missing documents, probate issues, unpaid taxes, strata problems, or slow administrative turnaround.

Mortgage purchase

3–6 months remains a fair planning range (sometimes longer), especially if valuation, credit checks, or title issues slow the process.

Commitment/approval timing can vary; some practitioners cite up to ~45 days in many cases depending on file readiness and lender queue.

7) Legal framework (Jamaica) — verified and slightly refined

Law / frameworkWhat it coversRegistration of Titles ActLand title registration and transfer process (Titles Office/Registrar of Titles).Stamp Duty ActStamp duty rules on instruments/documents (now commonly flat-rate in many relevant cases). Transfer Tax ActTransfer tax rules on real property transfers. Real Estate (Dealers and Developers) ActRegulation of real estate dealers/developers and the Real Estate Board. – REBProperty (Rights of Spouses) ActRights and division rules for spouses (family home issues). Mortgage Insurance ActFramework for government-backed mortgage insurance support (where applicable). Building Act (2018)Construction standards and regulatory framework; National Building Code direction. Land Valuation ActProperty valuation framework relevant to taxation/assessment contexts.National Housing Trust ActNHT contributions, benefits, and loan eligibility.Financial Institutions ActRegulation of banks/credit institutions.Common law / equity / case lawContract enforcement, deposits, specific performance, misrepresentation, etc.

Disclaimer: Strata purchases (apartments) also bring in strata-specific rules and fees; always have your attorney check the strata corporation status and arrears.

8) Practical tips

Don’t budget only for deposit. Budget for taxes/fees plus due diligence early, because delays often happen when people scramble for valuation/survey/legal payments.

Assume the Stamp Office can query value. If your price is far below market (family sale/gift), expect extra questions/valuation steps.

Use licensed professionals. The Real Estate Board regulates dealers/developers—verify licensing where possible.

Mortgage: compare lenders using written estimates. The “headline interest rate” isn’t the whole story—fees can differ a lot.

Expect administrative lag. Titles Office / stamping timelines can stretch; build slack into any move-in date.

Closing

Property transactions in Jamaica reward preparation. They favour those who understand not just the headline price, but the layers beneath it: the taxes assessed by the Stamp Office, the timelines imposed by lenders, the role of attorneys, surveyors, and valuers, and the quiet but decisive impact of documentation done properly — or not.

There is no single “standard” transaction. Every property carries its own history, every title its own nuances, and every buyer or seller their own priorities. What remains constant, however, is the structure within which these transactions take place. Once that structure is understood, the process becomes far less daunting and far more manageable.

Approached with the right advice, realistic timelines, and a clear grasp of costs, buying or selling a home in Jamaica can be a confident, well-ordered experience rather than an anxious one. And in a market that continues to evolve, that clarity is not a luxury — it is essential.

Frequently Asked Questions (2026)

Do I need a lawyer to buy property in Jamaica?

Yes — in practice and in law.

While Jamaican law does not use the phrase “mandatory” in casual terms, real estate transactions cannot be completed without licensed attorneys. Attorneys prepare and review the Agreement for Sale, conduct title searches and due diligence, manage stamping and registration, and ensure legal transfer of ownership. Attempting to buy property without legal representation is not realistic and exposes buyers to serious risk.

How long does a real estate transaction usually take?

This depends on whether the purchase is cash-funded or mortgage-backed, and on the condition of the title.

Cash purchases: typically 30–90 days, assuming a clean title and prompt responses from all parties.

Mortgage purchases: often 3–6 months, and sometimes longer if valuation, credit approval, or title issues arise.

Delays most commonly occur due to title defects, probate matters, unpaid taxes, missing documents, or lender processing timelines.

What does it typically cost to buy property in Jamaica?

There is no single fixed percentage, but buyers should plan realistically:

Cash purchases: buyer costs often fall in the region of 4%–6% of the purchase price, depending on legal fees and due diligence requirements.

Mortgage purchases: total buyer costs can rise to 9%–13% or more, once mortgage registration, lender fees, valuation, insurance, and additional legal work are included.

Important: Mortgage costs vary significantly by lender. Buyers should always request a written fee schedule or loan estimate before committing.

What costs does a vendor usually pay when selling property?

In a typical open-market sale where an agent is used, vendors often incur:

Transfer tax (2%)

Real estate commission (commonly around 5% + GCT on the commission)

Attorney fees and registration-related costs

As a result, total vendor costs can commonly fall in the range of 10%–12%, but this is not a statutory figure.

Costs may be lower in private sales or higher where legal or title complications exist.

Can I buy property in Jamaica while living overseas?

Yes. Many transactions are completed by overseas buyers every year.

However, buyers abroad should expect:

Longer timelines due to document notarisation, apostilles, or consular authentication

Reliance on power of attorney in some cases

Increased coordination between banks, attorneys, and courier services

It is strongly recommended to use an attorney experienced in overseas and diaspora transactions.

Can the government challenge the purchase price of a property?

Yes.

The Stamp Office and Tax Administration Jamaica may assess taxes based on market value, not only the stated purchase price — particularly in:

Family transfers or gifts

Undervalued transactions

Non-arm’s-length sales

Buyers and vendors should be prepared for valuation queries and possible reassessments.

Is a deposit always 10% of the purchase price?

Not always, but often.

A 10% deposit is customary in practice, but deposits are negotiable and ultimately governed by the Agreement for Sale.

Attorneys will ensure the deposit terms are legally sound and appropriate to the transaction.

Do I need approval to buy property in Jamaica if I am not a citizen?

No special government approval is required for most residential or commercial property purchases in Jamaica, whether you are a Jamaican, an overseas Jamaican, or a foreign national.

However, everyone involved in a property transaction must have a Tax Registration Number (TRN). This applies to locals and non-residents alike, and foreign nationals can legally obtain a TRN. A TRN is required to sign an Agreement for Sale, pay taxes, and register a transfer or mortgage.

Additional considerations may apply:

Purchases of agricultural land or very large tracts may attract extra scrutiny.

Banks often apply stricter lending requirements to non-resident buyers.

Non-resident buyers should obtain a TRN early and confirm financing rules in advance to avoid delays.

What are the most common causes of delay in Jamaican property transactions?

The most frequent issues include:

Defective or incomplete titles

Probate or estate administration delays

Outstanding property taxes or strata fees

Slow mortgage approvals or valuation delays

Missing or incorrectly executed documents

Early due diligence and professional advice significantly reduce these risks.

Final note on FAQs (2026)

These answers reflect current practice and legislation as at 2026, but real estate transactions are fact-specific. Fees, timelines, and requirements can change, and professional advice should always be obtained before committing to a purchase or sale.